![]() ING Global Economics Team

ING Global Economics Team

ING Economic and Financial Analysis

With ongoing political uncertainty, compounded by a tragic plane crash, South Korea's economic situation is rapidly deteriorating. There is no doubt that 2025 will be a challenging year for the South Korean economy. However, it could also be a year that showcases its resilience and strength in the face of political instability. Macro policies will be fully committed to stabilising markets and reviving the domestic economy, while exports will continue to be the backbone of the economy.

Worst year-end for the Korean economy

With the turmoil sparked by President Yoon Suk Yeol’s declaration of martial law on 3 December, the political situation has taken a turn for the worse. Both President Yoon (14 December) and acting President Prime Minister Han Duk-soo (27 December) were impeached. Deputy Prime Minister and Minister of Finance and Economy Choi Sang-mok has since assumed the role of interim leader, but his future remains unclear. Meanwhile, a tragic plane crash on 29 December prompted a national period of mourning until 4 January. The road to ameliorating political uncertainty and returning to normality is expected to be bumpy. Furthermore, the country also faces another major risk: trade and foreign policy uncertainty from the incoming Trump administration.

Amid ongoing political uncertainty at home and abroad, the won (-4.9% in December) and KOSPI (-2.24% in December) were the hardest hit during the year-end holiday season, and consumer and investment sentiment dampened significantly. December sentiment indicators for households and businesses are the worst since the global crisis in 2008 and the coronavirus pandemic in 2020. High-frequency data suggested a sharp decline in economic activity in early December, and the plane crash at the end of the month will further exacerbate the already poor economic activity and sentiment going forward. Hard data showed that all industry output in November slid for three consecutive months, but exports recorded another solid gain in December. Meanwhile, consumer inflation reaccelerated but remained below the Bank of Korea's target of 2%.

Against this backdrop, macroeconomic policies are expected to be fully dedicated to market stability to heal the wounds caused by political turmoil and to protect against a deterioration in sovereign creditworthiness. A sizable supplementary fiscal budget is expected to be announced to revive markedly diminished domestic growth, and monetary policy is expected to follow suit with faster rate cuts than we had expected.

Sentiment indicators deteriorated sharply in December and are likely to weaken further in the coming months

Source: CEIC

All industry production dropped for a third consecutive month in November

Even before all this bad news in December, overall economic activity was weakening. Mining and manufacturing industrial production fell -0.7% month-on-month seasonally adjusted in November (vs 0.0% in October, -0.5% market consensus). Semiconductor output rose (3.9%), yet car (-5.4%) and electronic parts (-4.7%) declined. Service activity also dropped by 0.2%, led by poor performances in finance and water/sewerage/waste disposal services. Meanwhile, retail sales rebounded 0.4% in November, but only partially offset the previous two months' declines (-0.3% in September, -0.8% in October). In terms of investment, both equipment investment (-1.6%) and construction investment (-0.2%) declined. Construction declined in 9 out of 11 months in 2024 and was the main drag on domestic growth. Yet, with construction orders bottoming out, we expect construction to rebound gradually in the middle of 2025. For equipment investment, capital goods imports have remained positive over the past few months and semiconductor-related investment is likely to continue. Facility investment is expected to grow modestly in 2025. In our view, services activity and private consumption are likely to be the hardest hit in the near term. However, as the current situation improves and with the help of accommodative monetary and fiscal policies, services and consumption are expected to gradually recover in the second half of 2025.

High frequency data suggests a further drop in activity

Source: CEIC

Exports are a bright spot in an otherwise gloomy economic landscape

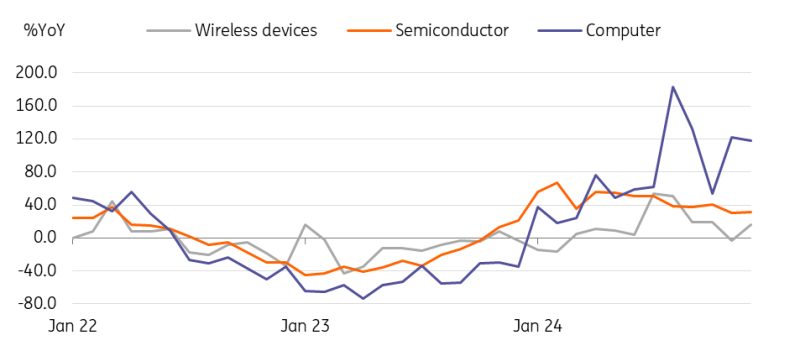

Exports grew 6.6% YoY in December (vs 1.4% in November, 3.8% market consensus), rising for 15 consecutive months. IT exports stand out, with significant increases in semiconductors (31.5%), mobile phones (16.1%), and computers (118%). Global demand for high-end memory chips such as HBM & DDR5 and SSDs remained solid as investment in AI increased. Meanwhile, reflecting sluggish global demand, general machinery (-7.0%) and petroleum (-12.2%) exports continued to decline. Car exports also dropped by 5.3% but mainly due to labour strikes and temporary production stoppages following a snowstorm. By destination, exports to China rose 8.6% with semiconductors, petrochemicals, and mobile phones seeing the most significant increases, likely due to some front-loading effect before the renewed tech-exports ban comes into effect in 2025. Exports to the US also rose 5.5% thanks to strong semiconductor exports, but exports of cars and general machinery, which are more closely linked to consumption, fell. Exports to the EU increased 15.1%. Car exports, the largest export item to the EU, dropped significantly, but vessel exports jumped 222.5%.

Meanwhile, imports rebounded 3.3% YoY in December (vs -2.4% in November, 2.7% market consensus). Energy imports declined -22.8% due to falling global oil and gas prices while non-energy imports rose 12.4%, led by a large increase of semiconductor-related imports (30.1%).

Strong IT exports continued in December

Source: CEIC

Exports to remain a bright spot despite growing trade tensions

We expect exports to remain a key growth driver for 2025, at least for the first half. Many are expressing concern about South Korea's exports this year. We too expect export growth to slow down to 4.0% YoY in 2025 compared to last year (8.4%). However, we expect some of Korea's strongest export categories to perform well despite rising trade tensions.

South Korean chipmakers have mostly focused on producing high-end chips that cannot be easily replaced by other players, and pre-orders for this year have already contracted. AI investment, led by the US, is expected to continue to rise steadily as there is still room for growth. However, tighter sanctions on exports to China and lower semiconductor prices will be the main factors behind a slowdown in semiconductor exports.

Ship exports are also expected to improve, driven by a boom in shipbuilding. Moreover, shipbuilding is probably the only industry that will be immune from Trump's tariffs and technology restrictions. Trump's defence strategy will require more investment in combat ships and Korean shipbuilders are the second largest combat shipbuilders after China (Please refer to our latest shipbuilding research: Asia shipbuilding renaissance). In addition, the ‘heavy-tail’ payment method, which typically sees 60% of the price paid upon delivery of the ship, could work in favour of South Korean shipbuilders. While this may increase the financial burden on shipbuilders in the early years of construction, the current trend of a stronger dollar could lead to an increase in KRW-denominated sales, boosting shipbuilders' profitability. Moreover, the number of ships to be delivered this year is likely to increase given the significant rise in orders in 2021 and 2022.

However, exports of automobiles, general machinery and oil, which are expected to be most affected by weakening global demand and changes in US policy are expected to decline in 2025. The weaker KRW could be a double-edged sword for exports, but the overall positive impact is likely to be slightly larger. While the negative impact on exports of SMEs focused on processing trade is likely to be somewhat greater, it is expected to be a positive factor for larger companies with diversified production bases and currency-hedging strategies. In addition, product categories that are losing price competitiveness to Chinese goods should also benefit from the weak KRW.

Inflation accelerated in December, but remains below the BoK's target

The consumer price index rose 1.9% YoY in December (vs 1.5% in November, 1.7% market consensus). The end of fuel tax cuts and higher global oil prices were the main reasons for the acceleration of headline inflation. Meanwhile, core inflation excluding food and energy eased to 1.8% in December (vs a November reading of 1.9%, which was also the market consensus). In a monthly comparison, headline inflation rebounded 0.4% MoM, nsa (vs -0.3% in November, and the 0.2% market consensus).

Going forward, we may see an acceleration of inflation mainly due to the weakening KRW, but sluggish domestic demand is likely to limit the increase. We expect core inflation, the BoK's preferred measure, to remain below 2% for a while. Thus, inflation conditions remain supportive of the BoK's expected rate cuts in the coming months.

GDP and CPI outlook

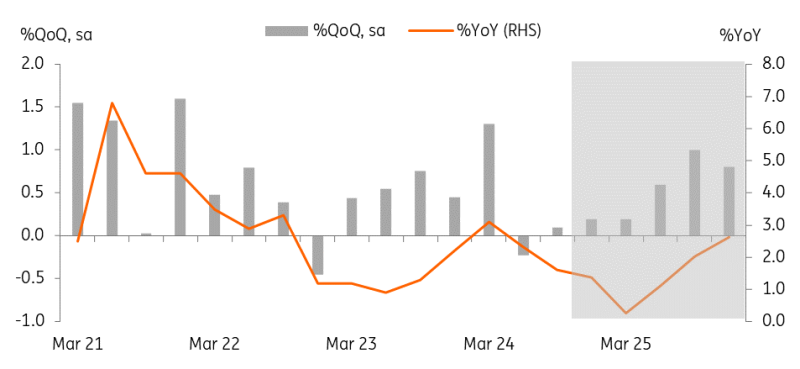

After analysing the latest data on production activity and sentiment indicators, we have lowered our GDP forecasts for 2024 and 2025 from 2.2% YoY and 1.6%, respectively, to 2.1% and 1.4%. Given the weaker-than-expected industrial production in November and the sharp deterioration in sentiment, we expect fourth quarter 2024 GDP to grow 0.2% QoQ sa (vs 0.1% in 3Q24). Despite the further weakening of domestic growth, a positive contribution from net exports should provide a buffer. Growth momentum should bottom out in 1Q25 (0.2%) and gradually pick up from 2Q25 onwards, as monetary easing and fiscal support kick in more meaningfully while sentiment recovers from the recent series of negative events. Exports will remain the main driver of growth in the first half of 2025, while domestic growth is likely to take the lead in 2H25. However, weak growth in the first quarter of 2025 will drag down the overall annual GDP growth for 2025.

On inflation, we maintain our current forecast of 1.7% YoY. While the weaker won has increased the upward pressure on inflation, the demand-side pressure has decreased amid sluggish domestic demand. We also expect the government to refrain from raising public service fees, citing economic stability.

Growth momentum will recover meaningfully in 2H25 with full support from monetary and fiscal easing

Source: CEIC and ING estimates

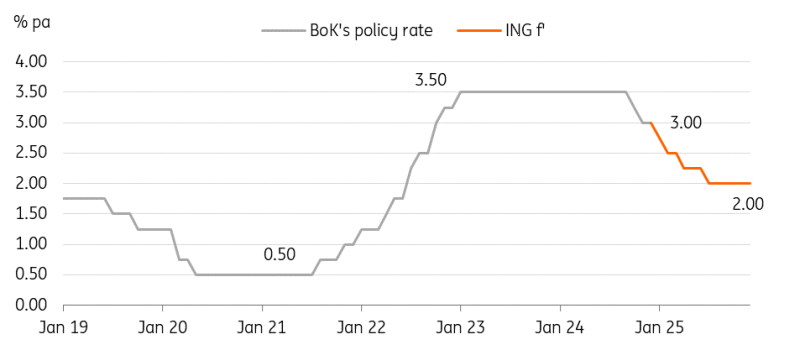

BoK watch: Front-loading of rate cuts in 1H25

Restoring consumer and business confidence will be a top priority for the Bank of Korea amid concerns about a weaker KRW and a widening rate differential with the Federal Reserve. We continue to believe that the BoK will cut by a total of 100bp in 2025, but the current situation will probably accelerate the pace of cuts.

Now, we expect a 25bp cut in both January and February. With political uncertainty lingering, downside risks to growth have grown faster than at the time of the November rate cut, increasing the need for the Bank of Korea to lower the policy rate below the neutral level quickly. Also, it will take a couple of quarters for the effects of the rate cut to feed through to the real economy, thus a faster pace of rate cuts is likely to maximise the policy impact.

As mentioned earlier, despite the weaker KRW, we still forecast core inflation to stay below 2% as sluggish demand anchors services prices. Household debt growth is likely to slow with heightened uncertainty ahead and the government's macroprudential measures. Rate cuts will ease the debt service burden, giving some breathing room for highly indebted households and businesses.

The BoK is expected to front-load rate cuts in 1H25

Source: CEIC and ING estimates

KRW outlook: The USD/KRW could possibly hit 1,500 in 1H25

Overall market conditions are likely to support a further weakening of the won. A slowdown in the pace of Fed rate cuts and escalation of trade tensions will likely add more depreciation pressure on the currency. Due to the strength of the dollar, it will be hard for the KRW to gain even if the domestic political condition improves. A widening yield gap and growth differentials between the US and Korea will probably push up the USD/KRW to the 1,500 level in the first half of 2025.

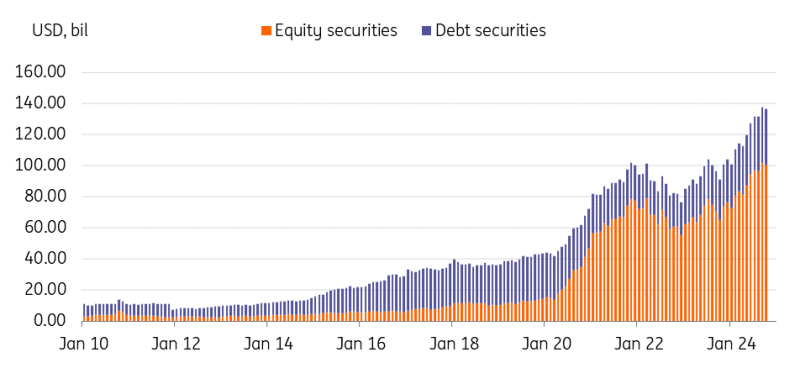

Recent USD/KRW movements have been largely driven by financial investment flows. Over the past few years, South Koreans' assets invested abroad have more than tripled. With the USD/KRW hovering around the 1,500 mark, we expect to see less appetite for overseas investments as the expected return of currency-adjusted investment declines. Considering that investment returns for large pension funds and institutional investors are mostly measured in won, the pace of overseas investment is likely to slow. On the other hand, Korean-denominated assets may become more attractive for foreign investors from a valuation perspective.

For these reasons, we have revised our quarterly projections of the USD/KRW. We now expect the KRW to close at 1,475 (1Q25), 1,500 (2Q25), 1,450 (3Q25), and 1,425 (4Q25). In terms of range, the KRW is expected to trade between 1,400-1,525 (previously 1,375-1,475).

Overseas investment by Korean residents has more than tripled since 2020

Source: SEIBRO

KTB issuance plan for 2025

The government announced KTB issuance plans for 2025 with a total issuance limit of 197.6tn won (excluding the foreign exchange stabilisation bonds of 20tn) and net issuance of 80tn. The government plans to place up to 60% of the issuance in the first half of the year (27-30% for 1Q25). By maturity, the government has allowed more flexibility for long-term tenors (20Y-50Y) to 35+/- 5% from +/- 3% last year, taking into account the demand conditions for lifers. In January, approximately 13.7tn won worth of KTBs and 0.8tn worth of won-denominated forex stabilisation bonds (for the first time since 2003) will be released.

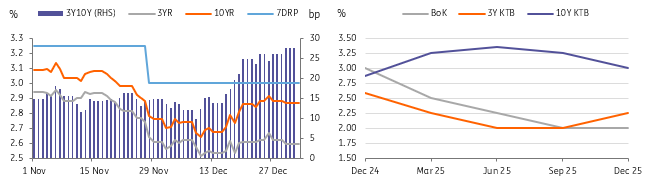

Rates outlook: All eyes are on the supplementary budget

Apart from the sharp depreciation of the won against the US dollar and increased volatility in the domestic stock market, the domestic bond market remained stable after the declaration of martial law and foreign funds continued to flow in. However, markets seemed to be starting to price in additional bond issuance, the question being when and how much. We expect a supplementary budget of around 10 trillion won to be approved for 1Q25 to prevent the economy from falling into recession and to stabilise livelihoods. Also, if the Supreme Court upholds the president's impeachment, both the ruling and opposition parties are expected to emphasise the need for expansionary fiscal policy during the presidential election campaign. In this case, an additional supplementary budget of around 15 trillion won is expected in the second half of 2025.

The supplementary budget is likely to trigger curve steepeners

Source: CEIC and ING estimates

Read the original analysis: Korea brief: What you might have missed over the year-end holiday

Aviso Legal: Esta publicación ha sido preparada por ING únicamente con fines informativos, independientemente de los medios, la situación financiera o los objetivos de inversión de cada usuario. La información no constituye una recomendación de inversión, ni es asesoramiento de inversión, legal o fiscal, ni una oferta o solicitud de compra o venta de ningún instrumento financiero. Más información: https://think.ing.com/content-disclaimer/

Últimos Análisis

CONTENIDO RECOMENDADO

El EUR/USD se deprecia ante la amenaza de Trump de mayores aranceles generales

El Euro sigue depreciándose a medida que el Dólar estadounidense se fortalece en mercados aversos al riesgo. El EUR/USD sigue cotizando a la baja, apuntando hacia el área de soporte de 1.1660.

Oro Pronóstico: La marea cambia a favor de los compradores del XAU/USD ante el aumento de las tensiones arancelarias

El Oro sube por tercer día consecutivo y busca registrar ganancias semanales el viernes.

Se espera una subida en la tasa de desempleo de Canadá, reforzando las expectativas de un recorte de tasas del BoC

Se espera que la tasa de desempleo en Canadá siga aumentando en junio. Un mayor enfriamiento en el mercado laboral podría favorecer recortes adicionales de tasas de interés.

El Euro cae a mínimos de 15 días, su descenso podría extenderse en las próximas horas

El quiebre del mínimo 1.1660 impulsará a la baja al par EUR/USD, que tendrá en su caso soportes en 1.1630 y 1.1605.

Forex Hoy: El Dólar estadounidense se beneficia de los flujos hacia refugios seguros

El Dólar estadounidense supera a sus principales rivales mientras los flujos de refugio seguro dominan la acción en los mercados financieros a primera hora del viernes, con el Índice del Dólar manteniéndose en territorio positivo por encima de 97.50 en la sesión europea. En la segunda mitad del día, Estadísticas Canadá publicará el informe de empleo de junio.